App Stores: the Latest Topic du Jour

By Ronald Gruia (News - Alert)

A recurring theme at CTIA (News - Alert) was the advent of the application store. In my previous MWC roundup article, I had already mentioned that app stores already had gotten quite a bit of attention in Barcelona, with the with launches from Nokia (News - Alert) (Ovi Store) and Microsoft (Windows Marketplace).

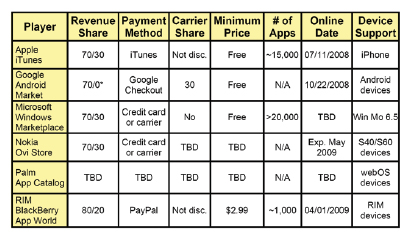

CTIA confirmed that trend, when RIM announced the availability of its own application storefront, BlackBerry (News - Alert) AppWorld (which had been originally announced this past October). Applications are already available for download in the US, UK, and Canada, and initially, they will be only for devices having a trackball or a touch screen. The company expects to have roughly 1,000 applications available on AppWorld for download over both cellular and WiFi (News - Alert) networks. RIM plans to apportion the revenues for applications sold through its storefront on an 80/20 basis with developers, which compares favorably with the 70/30 split for companies such as Apple (News - Alert), Google, Microsoft and Nokia (although it is important to note that Google passes the 30 percent balance for Android applications onto the operator). The accompanying table offers a quick at-a-glance view of all application store fronts.

The interest in app stores in not surprising, given the success of iPhone applications, which forced vendors such as RIM, Nokia, Palm, and Microsoft (News - Alert), among others, to follow suit. But there have been other catalysts that have also driven interest in app stores. One example is the proliferation of smartphones and QWERTY devices along with the growing popularity of touch have enriched the end-user experience in messaging and Internet surfing. Another factor is the advent of faster networks, which has driven data growth, which has been quite robust at 30-50 percent annually.

However, as LTE (News - Alert) looms over the horizon, the ROI for 4G services for operators who are in the "smart follower" category (rather than "early adopter" or avant garde) remains overhung in part because revenues are not growing exponentially with data traffic and the future business model is at risk if nothing changes. Data backhaul needs are almost exponential, potentially 3 times the voice cost (as presented by Telus’ CTO Ibrahim Gedeon in Barcelona at MWC), with wireless data demand increasing as prices decline.

In other words, we are facing a scenario in which data revenue and traffic are becoming decoupled, with service providers not attracting usage with content, but by data volume. This makes future 4G investments and cost structure somewhat difficult to justify with today’s data revenue model. So naturally, service providers are beginning to turn their attention to applications, and hence vendors are trying to meet that demand with the app stores. But will app stores by themselves do the trick? Some techie pundits are advocating a more horizontalized network that can allow operators to be more agile in the introduction of new services. But perhaps a change in the business model is also the answer, and there is a success story in Japan that corroborates that. NTT (News - Alert) DoCoMo’s i-mode service, which was launched back in 1999, features small screens and slow data rates (around 9.6 kbps). However, the i-mode business model was wide open, with APIs and SDKs being provided for third party developers to write new apps without any access restrictions.

The twist in the i-mode model was DoCoMo’s "bill-on-behalf" (which was essentially a 9% fee that the app developers paid to DoCoMo for billing services). This 2-sided business model proved to be a success, with over 100,000 new applications being introduced in over 3 years, and more than 15,000 apps using the billing service. This was the key behind NTT DoCoMo (News - Alert)’s success in data services (it has the highest data ARPU in the world).

Telcos have used 2-sided models in the past via toll-free (1-800 services available in the US and Canada). The Bell companies offered these services to enable businesses to connect with their customers and prospects and

enhance their customer care. However, there has not been much evolution in this vein since then, until the advent

of i-mode. As operators embark on the transition to the NGN, this approach can certainly offer some new interesting possibilities.

Ronald Gruia (News - Alert) is Program Leader and Principal Analyst at Frost & Sullivan covering Emerging Communications Solutions. Reach him at [email protected].

NGN Magazine Table of Contents

Internet Telephony Magazine

Click here to read latest issue

Internet Telephony Magazine

Click here to read latest issue CUSTOMER

CUSTOMER  Cloud Computing Magazine

Click here to read latest issue

Cloud Computing Magazine

Click here to read latest issue IoT EVOLUTION MAGAZINE

IoT EVOLUTION MAGAZINE