TMCnet News

Investor Group Issues "Proposals to Korea" to Help Increase Returns for Shareholders in Korean EquitiesA group of investors, led by Dalton Investments (supported by a group of investors) with holdings in select equities listed in Korea today issued the following abridged letter to the Korea National Pension Service and the Government, the National Assembly of the Republic of Korea: This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20190220005344/en/

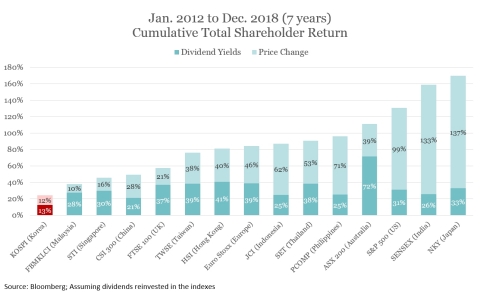

Source (News - Alert): Bloomberg; Assuming dividends reinvested in the indexes (Graphic: Business Wire) Dear Sirs and Madams, The Korean stock market is one of the worst performing and most undervalued markets in the world. Over the past seven years,1 KOSPI's2 total shareholder return3 was just 25%4 despite the fact that corporate profits5 increased by 80% over the same seven-year period. The Korea National Pension Service ("NPS"), which owns approximately 7% of the Korean equities market, and Korean individuals and institutions, which collectively own approximately 70% of the Korean market, have suffered greatly as a result of this sustained underperformance. The issue, however, extends to the entire country of Korea which is facing continuously slowing economic growth and the highest unemployment rate since 2001. While Korean companies have generated a great amount of value, this value has not been effectively transferred to Korean households and the economy. As a united front, the Korean Government, NPS and individual Korean shareholders and institutions have a tremendous opportunity to improve the Korea Discount and shareholder returns by collectively encouraging public companies to effect much needed change. As such, we urge NPS and the Government of Korea to implement initiatives which will strengthen the governance standards of Korean companies and thereby improve returns across the Korean equities market. I. Underlying Root Causes Chronic underperformance in the Korean equities market is driven by a systemic tendency of corporate management teams to pursue misguided capital allocation strategies, which inevitably ignore the interests of minority shareholders. This is clearly borne out by the numbers: The 5-year ('13-'17) average return on equity ("ROE") for Korean companies is one of the lowest in the world (including both advanced and emerging economies) at 9% (7% excluding Samsung (News - Alert) Electronics and SK Hynix)6, despite statistically higher capital expenditure (CapEx) levels in research and development and in businesses overall than any other market. Korean companies are putting far too little focus on return on capital, risk-adjusted returns and basic minority shareholder interests. The capital expenditure strategies these companies are pursuing yield revenue growth but at what cost? Far too often, companies make investment decisions based on affiliate companies and conglomerates instead of their own shareholders. We recommend that all capital allocation decisions be measured against the next best alternative (i.e., opportunity cost analysis), including share repurchases and dividend payouts, with an overarching objective to maximize long-term economic profit for all shareholders. Regarding payouts to shareholders, it has become all too common for Korean companies to accumulate what amounts to a treasure trove of assets, including cash that sits idle and unproductive on balance sheets. Given no better alternative, Korean companies should return this capital to shareholders so that capital can be allocated to other opportunities. Instead, Korean companies hoard cash. This has resulted in significantly below average payouts. By contrast, for example, Taiwan, a country which is economically similar to Korea, has an average dividend payout ratio of 58% compared to 17% for Korea. Taiwan's total shareholder return was 3 times more than that of Korea for the past seven years. As a result of this mismanagement, Korea's 5-year ('13-'17) average price to book ("PB") ratio is one of the lowest in the world, trading below 1.0x,7 which means investors actually expect Korean companies to destroy economic value. II. How to Fix It / Recommendations Implementing better capital allocation strategies and aligning management incentives with those of all shareholders could profoundly and positively impact the value of Korean companies and the wealth of countless Korean individual investors. As the largest single shareholder of Korean equities, NPS has the ability to drive and lead this change. About 17%8 of the portfolio of NPS is allocated to domestic equities, representing approximately $97 billion ininvestments. While NPS has generated a reasonable annual average return of 5.4%9, it has become difficult to generate high returns in this low interest rate environment. This will become an increasingly important issue as Korea's rapidly aging society is expected to accelerate the pension fund's depletion date. If structural changes are not implemented, which enable companies to achieve greater returns, NPS will have to increase the amount individuals contribute from their income to the fund by as much as 12-13% in the long-term and up to 38% in the very long term.10 We believe that the easiest way to ensure the stability and longevity of NPS - and to improve the economic vitality of the country - is to put in place proper governance guidelines that will improve the performance of the Korean equity market. Doing this will benefit retirement pension plans, Korean and foreign institutional and individual investors, as well as the country itself. Therefore, we recommend that NPS: 1. Focus on ensuring that any changes (e.g., payout increase) are measuring up to global standards and are sustainable.

2. Actively exercise shareholder rights as a steward of people's capital.

3. Focus on overall capital allocation and planning of companies to maximize long-term "economic value added" for all shareholders.

4. Changes screening metrics that determine target companies for shareholder return improvement.

5. Encourages its portfolio companies to prioritize share repurchases (including cancellation) over dividends when share prices are materially lower than estimated intrinsic value.

The Korean Government and National Assembly also have a role to play. Implementing initiatives that encourage better management of companies, and therefore enhanced growth, can dramatically improve the welfare of the country. Specifically, we propose: 1. Better alignment of tax rates to encourage fairer practices.

2. Make the electronic voting system and cumulative voting system mandatory and separate the audit committee's election.

3. Introduce a mandatory tender offer system that requires a potential buyer to not only make an offer to purchase shares held by the controlling shareholders but also make an offer to purchase shares held by the minority shareholders at the same price.

4. Relax certain excessive restrictions on capital allocation in regulated industries.

5. Encourage automatic investment system for retirement pension as the "default option"

Conclusion The chronic underperformance of the Korean equities market can be greatly improved if NPS uses its authority to implement stronger standards for capital allocation strategies and incentivizes Korean company management teams to pursue business initiatives that are in the best interests of all shareholders, not just majority shareholders. Capital allocation is resource allocation, and resource allocation must be efficient so that it is able to create more wealth for the country, its companies and people. If action is not taken now, this problem will only become more pronounced during a period of low growth, fierce competition, high unemployment, aging demographics and greater wealth inequality. As the largest shareholder of Korean equities, NPS has the power to push public companies to adopt better practices. We remain ready to constructively assist you and make ourselves available to discuss at your convenience.

Sincerely, Supported by (in alphabetical order): The supporting group agrees with the general messages above but not necessarily with every specific detail or argument. Brandes Investment Partners KCGI Ruane, Cunniff & Goldfarb Value Partners The full version of this letter and its accompanying presentation is available online at www.improvekorea.com. About Dalton Investments Dalton Investments LLC is a value-focused investment management firm with expertise in Asia equities, global equities and fixed income. Headquartered in Los Angeles, with a subsidiary office in Tokyo, Dalton manages $3.8 billion (November 30, 2018) in actively managed long-only and long/short strategies for pensions, endowments, foundations, financial institutions and family offices.

1 Source: Bloomberg (News - Alert)

View source version on businesswire.com: https://www.businesswire.com/news/home/20190220005344/en/ |