| [August 23, 2018] |

|

College is No Free Ride: One-in-Three Families Expect Kids to Save over $10K for College Costs by High School Graduation (but Haven't Told Them Yet)

How are American families coping with the sticker shock of college?

Although they will most likely be paying for new school supplies when

school starts this year, many parents-particularly those carrying their

own student debt-are asking kids to share more of the responsibility for

funding college. Findings from Fidelity

Investments'® 2018 College

Savings Indicator Study also reveal that although many

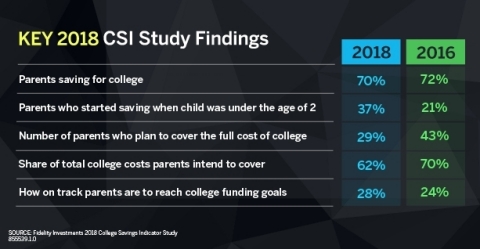

parents are saving earlier, it's still not enough: More parents are

starting to save before their child reaches the age of two-37 percent,

up from 21 percent in 2016-but are on track to meet just 28 percent of

their college funding goals. The good news: this important college

savings indicator is up from 24 percent in 2016.

This press release features multimedia. View the full release here:

https://www.businesswire.com/news/home/20180823005088/en/

Key 2018 CSI (News - Alert) Study Findings (Graphic: Business Wire)

Part of this improvement comes because parents expect their children to

take on a greater share of college costs. While still planning to cover

the majority of the costs (62 percent) themselves, the study found

parents want their children to set aside a whopping average of $15,385

by high school graduation, up from $12,431 in 2016. Similarly, fewer

parents feel it's their obligation to foot the whole bill for their

children's college (49 percent, down from 56 percent in 2016). (See

graphic on "Key 2018 CSI Study Findings.")

Considering these enhanced expectations, it's surprising that many

parents are delaying critical conversations with their children about

chipping in for college. In fact, 40 percent of parents with sophomores

or older haven't discussed with their kids that they're expected to

contribute to college savings, up from 31 percent in 2016.

"The study's findings are a sobering wake-up call for parents to improve

communications with college-bound kids," said Melissa Ridolfi, vice

president of Retirement and College Products at Fidelity. "It's no

wonder parents today are more realistic about how much they can

contribute to their kids' education, as nearly one in five are still

struggling to pay off their own student debt while saving for

retirement. Expecting children to assume more responsibility for college

costs makes sense-but the right time for the college talk is long before

the first tuition bill is due."

How much kids will be expected to pitch in isn't the only topic many

parents of 10th graders or older are putting off. (For a look

at other delayed conversations, see graphic on "Important talks parents

with 10th graders or above are delaying.")

Parents Need More Help on the Savings Front

Although the

survey reveals that 86 percent of parents feel they are better educated

about their finances having dealt with their own student loan debt, more

can be done to maximize college savings for their kids. Fifty percent of

parents admit they don't know the best accounts for college savings and

express uncertainty regarding exactly how much to save each month. One

possible factor: only 56 percent indicate they have a financial plan in

place to reach college savings goals, the lowest level since the

question was first asked in 2013. It's also a sharp decline from 2016,

when two in three parents had a plan in place.

As families look to get on track, advisors can play an instrumental role

in helping parents set up a clear college savings plan, and four in ten

respondents indicate they have a one-on-one relationship with a

financial professional to help make financial decisions (consistent with

2016 at 41 percent). A clear majority (64 percent) of families feel they

are closer to achieving their college saving goals thanks to the help of

their advisors. Further, when one compares families who have an advisor

against those who do not, those with an advisor demonstrate greater

confidence in their savings plans. (See graphic on "Achieving your

college saving goals.")

While having an advisor can potentially help families increase the

amount they put away each month for higher education, this year's study

uncovers several opportunities for advisors to add greater value by

discussing education goals and available savings strategies with family

members:

-

More than one out of three (34 percent) of families with advisors

haven't discussed 529 plans.

-

Only 29 percent said their financial advisor had discussed the

accelerated gifting option with them, down from 45 percent in 2016.

-

36 percent said their advisor did not meet with their child and 23

percent said their advisor did not provide them with information or

materials to discuss with their child.

"Clearly there is an opportunity for advisors to initiate a conversation

about college savings with both parents and their children," said Ron

Hazel, senior director of Fidelity Advisor 529 and individual retirement

products. "Advisors can help parents create savings plans and evaluate

investment strategies, but it's equally important to discuss those goals

directly with their children. These discussions an serve as a

foundation for younger family members' financial literacy as advisors

begin to build long-term relationships with the next generation of

investors."

Most Families Need Education about Recent 529 Tax Law Changes

Another

area where families need additional information is tied to recent tax

law changes enacted by Congress related to 529s, which allow holders to

use a portion of their 529 funds for K-12 tuition. Almost seven in 10

(69 percent) of parents are unaware of this change. Additionally, it's

uncertain how big an impact the change will have, with 30 percent

indicating it would not encourage them to open a 529 and almost one half

(49 percent) saying they weren't sure. Four in 10 of those with a 529

(or those who plan to open one) say it would not be used for K-12

tuition, while an additional one in four don't know. (Read this

Viewpoints article for information on whether the recent 529 tax

change makes sense for you.)

Tips and Resources to Help Parents Save More for College

For

parents looking for additional ways to defray college costs, respondents

share this advice: save as early as possible for college (46 percent);

open a dedicated savings account as soon as your child is born (28

percent); and treat saving for college like paying a bill for yourself

(26 percent).

Looking for more ways to boost your college savings? Fidelity has

additional resources available to help families:

-

Viewpoints

articles providing more insights on college topics, including: 5

lessons learned for college savings; Tips

for raising a saver; How

much college can you really afford? and a Student

loan guide. Additionally, developed for a younger generation of

parents who are constantly on-the-go, Fidelity.com/mymoney

offers short, interactive financial resources.

-

Fidelity's online College

Savings Quick Check calculator can show parents the impact of

saving a few extra dollars each month, based on their own timeline.

-

Fidelity's

College Savings Learning Center provides

a library of online resources for parents, including video courses on

saving account options and strategies and resources on more ways to

pay for college-such as how to apply for financial aid and

scholarships.

-

Asking friends and family to consider gifting to college savings for

birthdays or other holidays is becoming more common. To make

contributing easier, Fidelity offers a 529

Online Gifting Service, which lets owners of Fidelity's retail 529

college savings accounts encourage friends and family to help them

save for college.

-

In-person guidance from college planning representatives, available at

Fidelity's 197 nationwide investor

centers or by calling 800-544-1914. Fidelity also provides

financial advisor clients with 529 plan information, marketing support

and online tools such as the 529 State Tax Deduction Calculator and

the College Savings Planning tool. Financial advisors can get more

information at institutional.fidelity.com/529

or 1-800-544-9999

About the Fidelity Investments 2018 College Savings Indicator Study

As

part of the study, Fidelity conducted a survey of parents with

college-bound children of all ages. Parents provided data on their

current and projected household asset levels including college savings,

use of an investment advisor and general expectations and attitudes

toward financing their children's college education. Using Fidelity's

proprietary asset-liability modeling engine, the company was able to

calculate future college savings levels per household against

anticipated college costs. The results provided insight into the

financial challenges parents face in saving for college. Data for the

Indicator (number of children in household, time to matriculation,

school type, current savings and expected future contributions) was

collected by Boston Research Technologies, an independent research firm,

through an online survey from May 15 - June 15, 2018 of 1,899 families

nationwide with children aged 18 and younger who are expected to attend

college. The survey respondents had household incomes of at least

$30,000 a year or more and were the financial decision makers in their

household. College costs were sourced from the College Board's Trends in

College Pricing 2017. Future assets per household were computed by

Fidelity Personal and Workplace Advisors LLC (FPWA), a registered

investment adviser and a Fidelity Investments company. Within Fidelity's

asset-liability model, Monte Carlo simulations were used to estimate

future assets at a 75 percent confidence level. The results of the

College Savings Indicator may not be representative of all parents and

students meeting the same criteria as those surveyed for the study. For

more information, an Executive

Summary can be found on Fidelity.com.

About Fidelity Investment

Fidelity's mission is to inspire

better futures and deliver better outcomes for the customers and

businesses we serve. With assets under administration of $7.2 trillion,

including managed assets of $2.6 trillion as of July 31, 2018, we focus

on meeting the unique needs of a diverse set of customers: helping more

than 27 million people invest their own life savings, 23,000 businesses

manage employee benefit programs, as well as providing more than 12,500

financial advisory firms with investment and technology solutions to

invest their own clients' money. Privately held for 70 years, Fidelity

employs more than 40,000 associates who are focused on the long-term

success of our customers. For more information about Fidelity

Investments, visit https://www.fidelity.com/about.

Please carefully consider the plan's investment objectives, risks,

charges, and expenses before investing. For this and other information

on any 529 college savings plan managed by Fidelity, contact Fidelity

for a free Fact Kit, or view one online. Read it carefully before you

invest or send money.

The UNIQUE College Investing Plan, the Fidelity Advisor 529 Plan, the

U.Fund® College Investing Plan, the Delaware

College Investment Plan and the Fidelity Arizona College Savings Plan

are offered by the state of New Hampshire, MEFA, the state of Delaware,

and the Arizona Commission for Postsecondary Education, respectively,

and managed by Fidelity Investments. If you or the designated

beneficiary are not a New Hampshire, Massachusetts, Delaware or Arizona

resident, you may want to consider, before investing, whether your state

or the designated beneficiary's home state offers its residents a plan

with alternate state tax advantages or other benefits.

Units of the portfolios are municipal securities and may be subject

to market volatility and fluctuation.

Fidelity, Fidelity Investments, Fidelity Advisor Funds, and the

Fidelity Investments & Pyramid Design logo are registered service marks

of FMR LLC.

The third party marks appearing herein are the property of their

respective owners.

Boston Research Technologies is not affiliated with Fidelity

Investments.

855539.1.0

© 2018 FMR LLC.

View source version on businesswire.com: https://www.businesswire.com/news/home/20180823005088/en/

[ Back To TMCnet.com's Homepage ]

|